The rise of generative AI is not simply another search update. It represents a structural reconfiguration of how value moves across the web.

For more than two decades, the internet operated on a relatively stable economic bargain. Publishers created content, search engines indexed it, and users discovered information by clicking through to the original source. Traffic served as the currency connecting content creation to monetization. But that model is now under pressure.

Google's AI Overviews, the rollout of AI Mode, and the rapid adoption of conversational search systems are gradually transforming search engines from referral platforms into destination platforms. Instead of directing users toward websites, they increasingly satisfy informational intent within their own interfaces. The result is a subtle but profound shift. Visibility and traffic are no longer synonymous.

For publishers whose business models depend on advertising, affiliate revenue, subscriptions, or lead generation, this may prove to be one of the most consequential platform changes since the emergence of Google Search itself.

The scale of the transition is difficult to ignore. Gartner projects that traditional search volume could decline by 25 percent by the end of 2026, while longer-term forecasts suggest that more than half of all search activity may eventually migrate toward AI-mediated environments. Whether those projections prove perfectly accurate is almost secondary. The direction of travel has become increasingly clear.

At the same time, a new optimization industry has emerged almost overnight. Generative Engine Optimization, largely unknown a few years ago, is expected to grow into a multibillion-dollar market before the end of the decade. Entire teams are now dedicated to influencing how AI systems cite, summarize, and surface information.

Markets rarely form around temporary phenomena. They form around structural shifts. Google's own numbers point in the same direction. AI Overviews now reach billions of users globally, while AI Mode continues its international expansion. As answer generation becomes integrated directly into the search experience, the traditional sequence of search, click, and website visit begins to fragment.

The web is slowly moving from a discovery architecture toward an extraction architecture. Information is still created by publishers, but increasingly consumed elsewhere.

For years, discussions about zero-click search remained largely theoretical. That is no longer the case. The impact of AI-generated answers can now be measured across multiple independent datasets, and despite methodological differences, the conclusions are remarkably consistent.

A large-scale study by the Pew Research Center found that users clicked traditional organic search results roughly 15 percent of the time when no AI-generated answer appeared. Once an AI Overview was present, that figure dropped to just 8 percent; more notably, over a quarter of searches ended without any external click at all.

Similar patterns appear across commercial SEO datasets. Research from Ahrefs, based on 300,000 keywords, found a 34.5 percent reduction in expected click-through rate for the first organic result after AI Overviews appeared. SISTRIX reported an even steeper decline in Germany, estimating that top-ranking results lost almost 60 percent of their historical click share. Seer Interactive reached comparable conclusions across a dataset of 25 million impressions.

The precise percentage varies by query type, industry, and market. The broader conclusion does not. AI-generated answers consistently reduce the probability that a user will visit the originating source.

| Study / Source | Keyword / Data Basis | Position 1 CTR Loss | Industry Impact |

|---|---|---|---|

| Pew Research Center | 68,879 searches, 900 US adults | Click rate drops from 15% to 8% in the presence of AI Overviews | 26% of searches end without a click directly on the SERP |

| Ahrefs Analysis | 300,000 keywords | -34.5% relative CTR decline on position 1 | Rise of zero-click searches and high citation dilution |

| Seer Interactive | 25 million impressions | CTR drops from 1.76% to 0.61% (-61% to -65%) | Paid search ads fell from 19.7% to 6.34% CTR (-68%) |

| SISTRIX Germany | 100 million keywords | CTR drops from 27% to 11% (-59%) | Monthly loss of 265 million clicks for German websites |

| Digital Content Next | 19 premium publishers | N/A | Median decline of Google referral traffic by 10% YoY |

What makes these findings particularly significant is that the effect extends beyond normal ranking volatility. Ahrefs attempted to isolate the influence of AI Overviews by comparing actual performance against projected CTR curves derived from control groups. The resulting gap suggests that a substantial portion of the decline cannot be explained by changing rankings or seasonal fluctuations alone. It represents traffic that previously flowed to publishers but now remains within Google's own interface.

This distinction matters because it changes the competitive landscape. Publishers are no longer competing solely against other publishers. They are increasingly competing against the search layer itself.

Not all searches are affected equally. The strongest impact appears in precisely the areas where publishers have historically generated the greatest volume of evergreen traffic.

Short navigational searches still produce relatively few AI responses. Complex informational queries produce far more. Long-form questions, natural language searches, and explicit informational requests frequently trigger AI-generated summaries before users ever encounter a publisher's website.

From Google's perspective, these are ideal use cases. The answer can often be synthesized from existing sources without requiring additional navigation. From a publisher's perspective, however, these same queries have traditionally been among the most valuable opportunities for audience acquisition.

The paradox is difficult to miss. The content categories that search engines once rewarded most aggressively are now often the easiest to summarize away.

Perhaps the most important development is not the decline in clicks itself, but the decoupling of visibility from economic value. Historically, rankings functioned as a reliable proxy for traffic. Publishers invested in content, earned visibility, and received visitors in return. The relationship was imperfect, but it was predictable.

AI-generated answers weaken that relationship. A publisher may still provide the underlying information. It may still be cited. It may even maintain strong rankings. Yet a growing share of user intent is resolved before the click occurs. This represents a fundamental change in how content is monetized online.

For years, the dominant risk for publishers was failing to rank. Increasingly, the dominant risk may become ranking successfully while receiving only a fraction of the traffic that those rankings once produced.

The effects are not distributed evenly across the digital economy. Publishers focused on informational content appear particularly exposed, as their content closely aligns with generative systems' strengths. Technology, SaaS, health, education, and financial websites have all reported significant declines in traffic as AI-generated answers become more prevalent.

Data collected by Digital Content Next from major publishers suggests that referral traffic from Google began to decline measurably in 2025. Evergreen content brands experienced some of the steepest losses, while news organizations generally showed greater resilience due to their reliance on timeliness and original reporting. This distinction may become increasingly important.

AI systems excel at compressing established knowledge. They remain considerably less effective at generating original reporting, exclusive research, firsthand experience, and proprietary data.

In practical terms, publishers whose business models depend primarily on summarizing existing information may face greater pressure than publishers producing genuinely scarce information. The economic value of originality appears to be rising precisely because AI has made summarization abundant.

Yet the situation is more nuanced than simple narratives of traffic decline suggest. Several studies indicate that visitors arriving via AI-mediated discovery often exhibit stronger intent than those arriving through traditional search. Research from the Kellogg School of Management found higher engagement rates and stronger conversion behavior among users referred through AI-driven pathways.

This phenomenon creates what could be described as a Citation Traffic Paradox. Publishers lose volume but gain qualification. AI systems increasingly act as behavioral filters. Casual information seekers receive their answers immediately and never click. Users who continue toward the source often do so because they need deeper expertise, validation, purchasing guidance, or additional context.

Traffic becomes scarcer, but potentially more valuable. Whether this quality improvement can compensate for the broader volume losses remains an open question. For most publishers today, the answer is probably no. But it hints at a future in which audience quality matters more than audience size.

That possibility becomes even more apparent when examining individual case studies across the publishing ecosystem.

| Device Class & Region | CTR without AI Overview | CTR with AI Overview | Net Click Rate Decrease |

|---|---|---|---|

| UK Desktop | 25.23% | 2.79% | -89.0% |

| UK Mobile | 25.23% | 3.28% | -87.0% |

| US Desktop | 25.23% | 3.78% | -85.0% |

| US Mobile | 25.23% | 3.28% | -87.0% |

The most important question facing publishers today is no longer whether AI reduces traffic. The evidence for that is already overwhelming. The more consequential question is what replaces the referral economy once traffic stops functioning as the primary mechanism for distributing value across the web.

A growing number of signals suggest that the industry is moving toward an entirely different model. Instead of earning value through clicks, a small group of publishers increasingly monetize their content through direct licensing agreements with AI companies.

The result may be the emergence of a two-tier internet. One layer produces content for the open web and competes for shrinking volumes of referral traffic. The other supplies proprietary data directly to AI platforms through commercial agreements that bypass traditional search entirely.

Few companies illustrate the risks of platform dependence more clearly than Chegg. For years, the educational platform built its growth model around a straightforward assumption. Students searched for academic questions, discovered Chegg on Google, and became paying customers. That assumption broke down surprisingly quickly.

According to figures disclosed during litigation against Google, Chegg lost nearly half of its non-subscriber organic traffic within a single year. The timing closely mirrors the rollout of increasingly sophisticated AI-generated answers that can solve educational and mathematical queries directly within search results.

Whether Google's conduct ultimately violates competition law remains a question for courts. The economic reality is easier to observe. When a platform can answer the question itself, intermediaries that previously monetized the answer become vulnerable. Chegg may be one of the first large-scale examples of a challenge that will likely extend far beyond education.

While many publishers struggle with declining traffic, a different strategy is emerging among the largest content platforms. Rather than fighting AI systems, they are beginning to sell access to them.

Reddit, Stack Overflow, Reuters, Axel Springer, and numerous other content owners have entered licensing agreements that transform decades of accumulated content into machine-readable infrastructure for large language models.

This development represents a significant departure from the original logic of the web. Historically, content generated value when users visited the source. Increasingly, content generates value when machines consume the source.

Reddit offers perhaps the clearest example. After years of operating as an open platform, the company aggressively restricted access for crawlers and negotiated direct licensing agreements with both Google and OpenAI. At the same time, Google's search algorithms dramatically increased Reddit's visibility, helping offset broader changes in search behavior. The result is striking. Reddit increasingly earns revenue from human attention as well as from machine consumption.

Stack Overflow has followed a similar path. After experiencing a dramatic decline in user activity following the arrival of ChatGPT, the company repositioned itself as a structured knowledge provider for AI systems. Rather than relying exclusively on community traffic, it now monetizes expert knowledge through APIs and commercial partnerships.

Both examples point toward the same conclusion. The future value of content may increasingly depend on ownership of unique datasets rather than ownership of pageviews.

| Licensee / Partner | Agreement Volume | Contract Type & Duration | Primary Content |

|---|---|---|---|

| Reddit (Google) | ~$60,000,000 / year | Fixed licensing fee (2024–2027), transition to dynamic pricing planned | Real-time access to all user-generated forum content for model fine-tuning |

| Reddit (OpenAI) | ~$70,000,000 / year | Multi-year contract | Provision of structured user data for ChatGPT training purposes |

| Axel Springer (OpenAI) | ~€25,000,000 / year | Ongoing licensing payments | Use of historical publisher archives and integration of current news summaries |

| Reuters (OpenAI) | ~$65,000,000 total volume | One-time payment ($25M) + $40M distributed over three quarters | Access to global news archives and agency feeds |

| Dotdash Meredith (OpenAI) | ~Min. $16,000,000 / year | Continuous partnership | Licensing of niche and advice content for ChatGPT evaluation |

| Corint Media (Google) | ~€3,200,000 / year | Interim agreement (following DPMA arbitration) | Compensatory payment for the use of the press publisher's intellectual property rights in Germany |

Not every publisher can negotiate multimillion-dollar licensing agreements. That reality introduces a growing asymmetry into the publishing ecosystem. Large platforms with strong brands, proprietary archives, and enormous content inventories possess leverage. Smaller publishers often do not.

The danger is that AI systems concentrate value in the hands of a relatively small group of content owners while reducing monetization opportunities for everyone else. In such a scenario, the open web risks becoming economically unsustainable for independent publishers, even as their content continues to contribute to the broader AI ecosystem.

This is one reason why tensions between publishers and AI companies continue to escalate. The conflict is no longer primarily technological. It is increasingly economic.

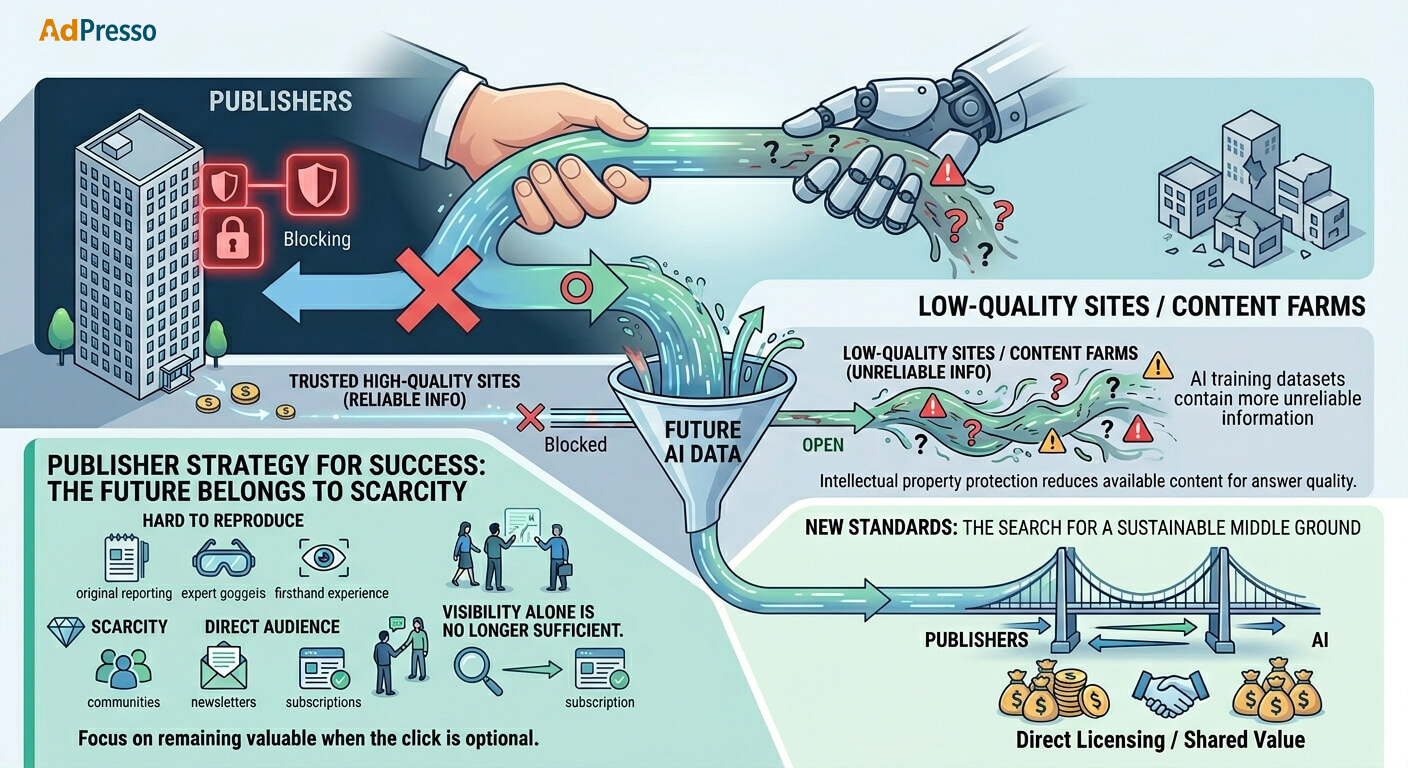

Publisher resistance is becoming visible at the infrastructure level. Across major news organizations, blocking AI crawlers has shifted from an exception to a default policy. Most large publishers now restrict at least some form of AI data collection, while a growing number prohibit all major AI crawlers entirely. The motivation is straightforward.

Publishers increasingly view unrestricted crawling as a one-sided exchange in which valuable content leaves their websites without generating meaningful traffic in return.

Cloudflare's crawler analysis illustrates the imbalance particularly well. In some cases, AI systems generated tens of thousands of content retrieval requests for every single visitor they sent back to the originating publisher. This ratio exposes the central tension of the AI era. The traditional search economy depended on reciprocity. Crawling generated visibility, and visibility generated traffic.

The emerging AI economy often breaks that relationship. Content continues to be extracted. Referral value frequently disappears.

The growing wave of crawler blocking creates another challenge that receives far less attention. High-quality publishers are often the first organizations to restrict access. Low-quality websites frequently remain completely open.

Researchers have already identified signs of this imbalance. Trustworthy publishers increasingly exclude AI crawlers, while misinformation networks and low-quality content farms continue to supply data without restriction.

If this pattern persists, future AI training datasets may gradually contain a larger proportion of unreliable information. Ironically, the same publishers attempting to protect their intellectual property may inadvertently reduce the availability of the very content that helps maintain answer quality.

The long-term consequences remain uncertain, but the incentive structure appears increasingly problematic.

| AI Crawler / User Agent | Operating Company | Disallow Share of Global Crawler Traffic | Net Sentiment (Ratio of Allow to Disallow) |

|---|---|---|---|

| GPTBot | OpenAI | 5.52% | Balanced (Very frequently blocked but also often explicitly allowed) |

| CCBot | Common Crawl | 5.08% | Predominantly negative (Almost exclusively blocked) |

| ClaudeBot | Anthropic | 4.88% | Slightly negative (Blocked more frequently than allowed) |

| Google-Extended | 4.44% | Slightly negative (Blocked more frequently than allowed) | |

| Bytespider | ByteDance | 4.23% | Predominantly negative (Block rate significantly exceeds allowances) |

| Meta-ExternalAgent | Meta | 3.82% | Negative (Never explicitly allowed in analyses) |

| Amazonbot | Amazon | 3.80% | Negative (Blocked almost without exception) |

| Applebot-Extended | Apple | 3.67% | Negative (Blocked almost without exception) |

The industry's response is beginning to evolve beyond simple blocking. Organizations such as the IAB Tech Lab are developing frameworks to transform content access into a standardized, monetizable process. Emerging initiatives focus on authentication, licensing, attribution, and pay-per-crawl models that would allow publishers to participate more directly in the value generated by AI systems.

Whether these efforts succeed remains unclear. What is clear is that the current model satisfies neither side particularly well. Publishers argue that compensation remains inadequate, while AI companies face growing legal, technical, and political resistance. The search for a sustainable middle ground has effectively become one of the defining infrastructure challenges of the modern web.

For publishers, the strategic implications are becoming increasingly visible. The content most vulnerable to AI disruption is also the content that dominated SEO strategies for much of the last decade. Generic informational articles, surface-level explainers, and easily summarized content are steadily losing economic value.

Content that gains value tends to share a different characteristic. It is difficult to reproduce. Original reporting, proprietary datasets, expert analysis, firsthand experience, community-driven insights, interactive tools, and unique research create forms of scarcity that AI systems cannot easily commoditize.

This does not mean SEO becomes irrelevant. It means that visibility alone is no longer sufficient.

The publishers most likely to thrive in the next decade will be those that treat search as one distribution channel among many rather than the foundation of their entire business model. They will invest in newsletters, communities, subscriptions, direct relationships with audiences, and differentiated expertise.

The open web is unlikely to disappear. But the economic assumptions that shaped it for the past twenty years are already beginning to change. The central question for publishers is no longer how to rank. It is how to remain valuable when the click itself becomes optional.